|

|

The similar process but without trend is the LM-Aff-Mic-ARCH process. The overall introduction for the processes with trend is given in the description for the GARTCH(1,1) process.

For the multi-component processes with trend, the historical volatilities σk are computed as without trend. The effective volatility is modified to add the effect of the past trends at the time horizons present in the process

r[lk](t - lkδt) (1)

k=1 k=1

∑

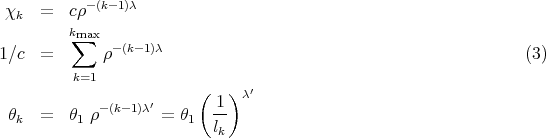

wk = (1 - w ∞ )χk with χk = 1 (2)

k](description0x.png)

The parameters for the simulations are

The innovations have a Student distribution with 3.3 degree of freedom. The simulation time corresponds to 200 years with a time increment δt = 3 minutes.