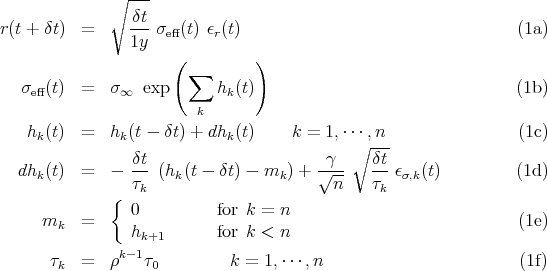

Long Memory exponential stochastic volatility process

The long memory exponential stochastic volatility model with n components is

defined by:

The parameters of the process are σ∞, τ1, τn, γ and the PDF for ϵr and

ϵσ,k.

The various terms are:

δt: the time step for the discrete process. The term ’1y’ denote the one year time interval, and the factor

brings the annualized volatility σeff to the scale δt.

ϵr: random variable, with zero mean and unit variance.

σ∞: Proportional to the annualized volatility (up to correction in

exp(< h2>)).

τk: The characteristic time of return for hk(t) toward the mean mk.

mk the mean term for the logarithmic volatility. In this model, the mean volatility at a given scale k is the volatility

hk+1 at the longer scale k + 1.

γ: The strength of the volatility noise. This parameter fixes the

vol-of-vol.

ϵσ,k: random variable, with zero mean and unit variance. For the simulations, the distribution is a Student with 3.0 degree of

freedom.

brings the annualized volatility σeff to the scale δt.

brings the annualized volatility σeff to the scale δt.