| |

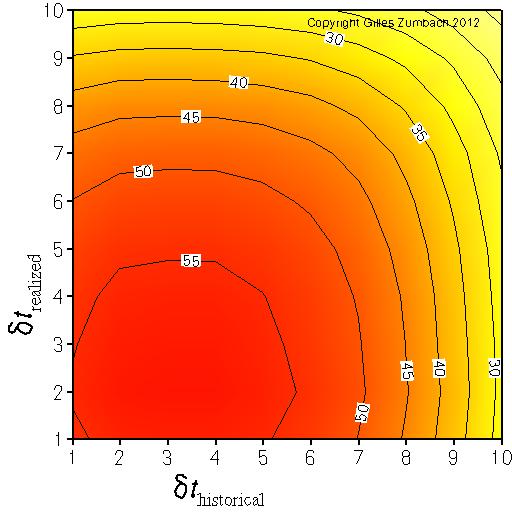

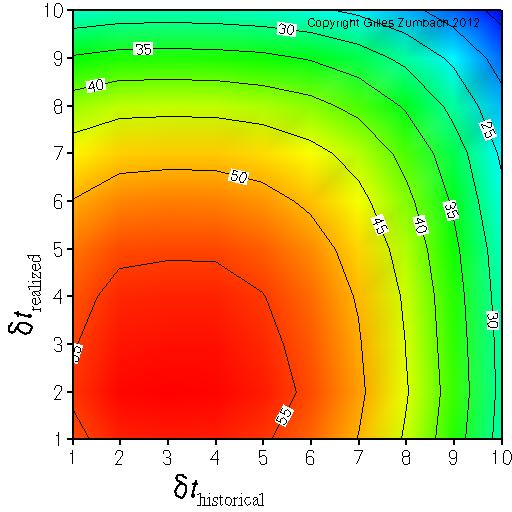

The lagged correlation between fine and coarse grained volatilityThe axises gives the logarithm (base 2) of the return time horizons dt used to compute the volatility. |

|

|

|

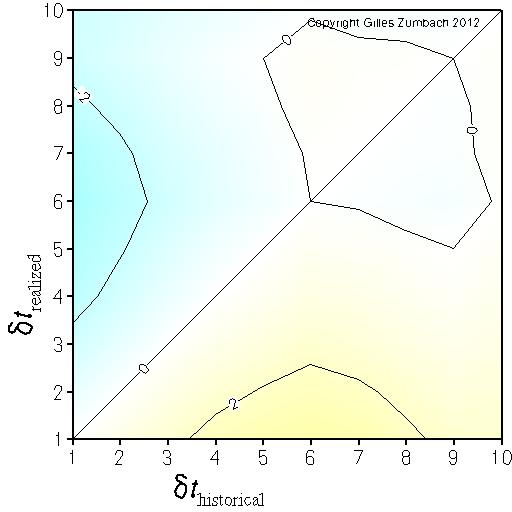

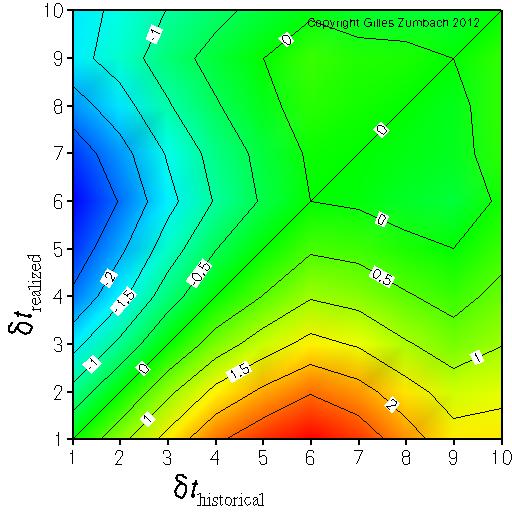

Asymmetry for the lagged correlation between fine and coarse grained volatilityThe axises gives the logarithm (base 2) of the return time horizons dt used to compute the volatility. |

|

|

|