|

|

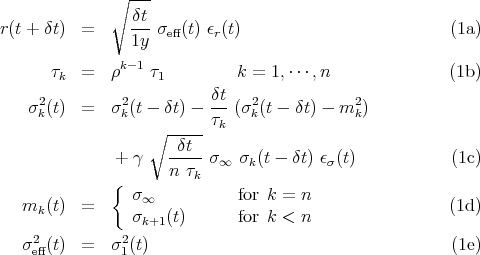

The long memory Heston process is a minimal modification of the Heston process so as to introduce a volatility cascade. The equations for the model with n components are:

where all the volatilities σ∞, σeff(t) and σk(t) are annualized. The parameter σ∞ fixes the mean annualized volatility, the vector τk sets the mean reversion time for σk, and γ is the noise level for the volatility. The equations for the volatility are iterated starting from k = n and decreasing, so as to incorporate in the scale k the new information at the scale k + 1 at the time t.

The parameters for the simulations are:

The simulation time corresponds to 200 years with a time increment δt = 3 minutes.